Business Visualizations

Study Shows Three Decades of Self-Employment Trends

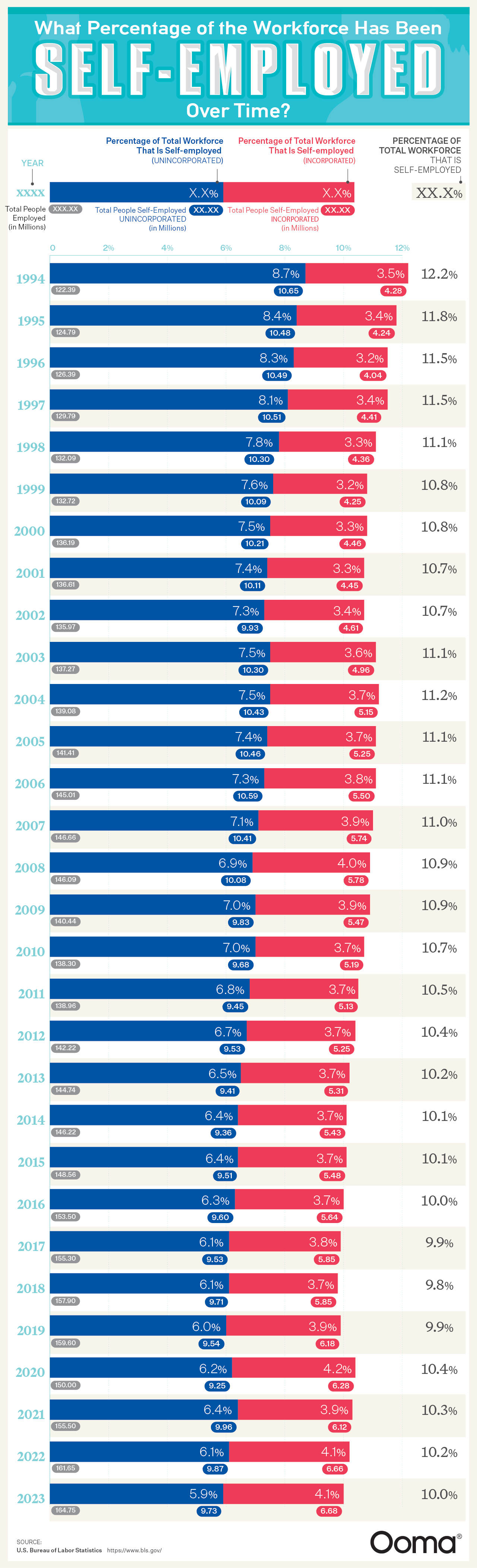

The U.S. economy and workforce landscape have seen many dramatic changes in the past three decades, not just in terms of trends, crises, and types of jobs workers pursue, but also in the way we work and structure careers. The team at Ooma created a new study displaying trending changes in self-employment. Their chart shows the percentage of the workforce that was self-employed each year. The numbers show that self-employment has always played a strong role in the American economy, with new Internet and digital industries pushing it to evolve. These changes present new opportunities and shake-ups to old work patterns.

Click below to zoom.

The Rise and Fall of Traditional Self-Employment

Ooma’s analysis is based on data from the U.S. Bureau of Labor Statistics. It shows that in 1994, self-employment represented 12.2% of the workforce. That’s 14.93 million Americans, a peak representing an economy where entrepreneurs, freelancers, contractors, and trades workers formed the backbone of the economy.

The next two decades saw a shift in self-employment, however. It declined to 9.8% by 2018, representing a shift to corporate employment in the era of social media and dot-com booms. The economy was recovering from a major recession that affected self-employed workers. Workers needed stability and benefits, and they turned away from gig work during the recession, with numbers plummeting to 59% in 2023.

The Impact of the Internet

Smartphone technology was developed in the late 1990s and perfected throughout the 2000s until it became a force that transformed the way we work. New apps like Uber, Instacart, and DoorDash ushered in a huge demand for gig work in the form of delivery drivers and people who could transform their own car into a taxi service. These platforms offered many work opportunities on top of a flexible schedule. People using these apps to get jobs could work whenever they wished.

Social media offered other exciting self-employment opportunities as we watched the rise of influencers and content creators who could market all kinds of digital goods and other services. A digital ecosystem made it more possible for personal brands to affordably market themselves to a wider audience.

The Pandemic as a Catalyst

The COVID-19 pandemic prompted huge changes in the way we work. Businesses closed down, layoffs surged, and many people looked for the quickest way to get flexible new employment. Self-employment options were the most accessible for many people. The self-employment workforce rose again to 4.2% in 2020. Many began to feel that starting their own business was more reliable than trusting a corporation. Marginalized people were especially drawn to self-employment, particularly women with families, and Black and Hispanic women. The flexible scheduling and greater power over work decisions was a more equitable fit for these women.

The team’s data proves that self-employment is so much more than just an alternative career choice. It can be an equalizer and drive American innovation. Self-employment can be a huge boost to local communities and continues to serve a vital role in our economy.

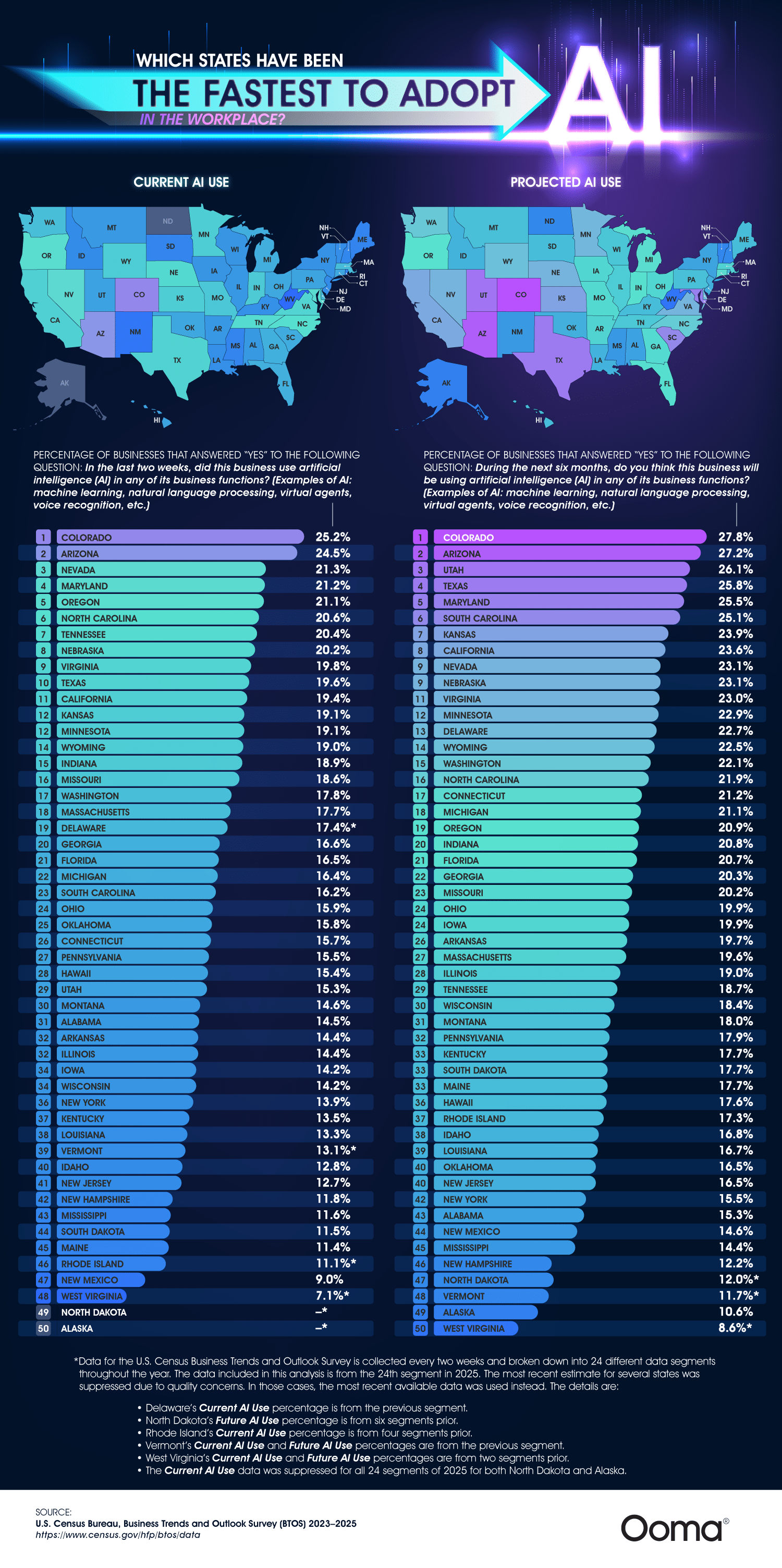

AI is spreading rapidly, especially in the workplace. According to surveys, 46% of American workers have used AI a few times in the past year. As the AI industry rapidly expands, Ooma examined how quickly U.S. states are adopting artificial intelligence in the workplace with a data-driven snapshot of current usage and future expectations. Using U.S. Census Bureau survey data, the team’s work highlights geographic trends and broader implications for business as AI becomes more enmeshed in daily business dealings.

Click below to zoom.

The team’s research ranks states on two key metrics: current AI adoption (whether businesses have recently used AI tools) and projected adoption (whether businesses expect to use AI in the near future). These combined elements allow us to see not only where AI is already in use, but where momentum is building. The infographic provides a visual way to compare states and identify these patterns.

One of the most striking findings is that Colorado, Arizona, and Nevada lead the way in the current AI usage. Over one-fifth of his businesses have recently adopted AI. Colorado stands out as a top state, with 25% of businesses already using AI in some capacity. These tools can include machine learning, virtual assistants, natural language processing, and other AI capabilities, supplementing everyday business tasks such as data analysis, communication, and customer service.

The map also reveals that the same states dominate in projections for future AI use. Colorado and Arizona take top rankings once again. This suggests that early adopters are more likely to keep investing in AI and remain in their leadership positions. States like Utah and Texas ranked highly in future projections, indicating these are emerging areas for AI growth.

We can see states on the opposite end of the spectrum, lagging behind the leaders. West Virginia, Alaska, and parts of the Northeast report much lower levels of current and anticipated use. Even though it’s an economically robust and influential state, New York ranks low for adoption, showing that size and economic power don’t always indicate rapid AI growth.

The team’s work suggests that differences might be influenced by factors like industry composition, workforce skills, and access to tech infrastructure. States with strong technology sectors and a growing startup economy are the most likely to adopt AI quickly, while states with more traditional economies and heavy reliance on physical labor might have slower transitions.

Remember that AI adoption is still in the early stages. Even in leading states, only one in four businesses reports using AI, so there’s still a lot of room for growth. This aligns with broader trends showing AI is expanding rapidly, but it hasn’t yet reached saturation.

The article paints a picture of a fragmented but rapidly spreading AI landscape in the U.S. While some states lead the charge, widespread adoption is still rolling out and could shake up these rankings a lot in the coming years.

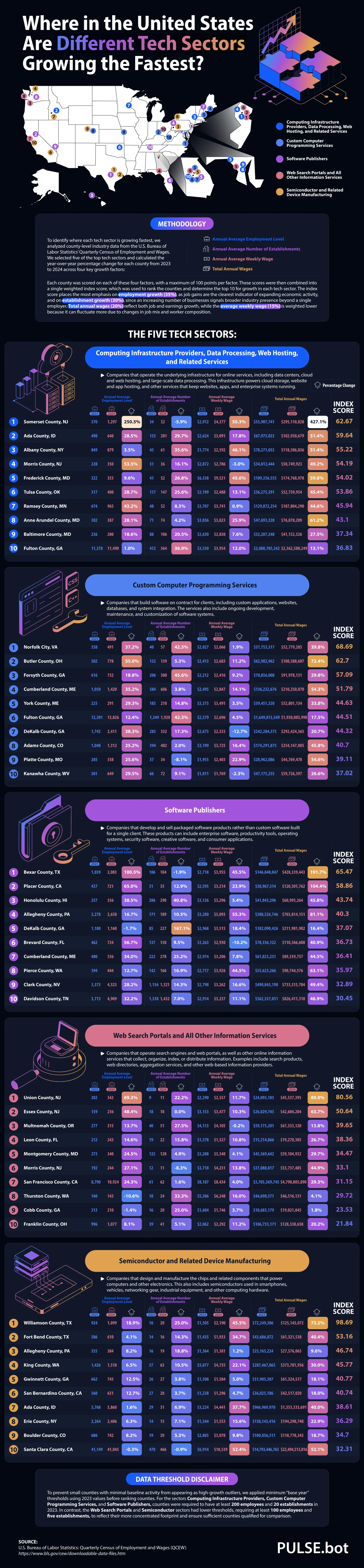

Tech is one of the world’s biggest industries, with many of the dominant Fortune 500 tech companies based in the United States. Four tech companies alone are worth trillions of dollars, and though the industry is full of rapid changes, it’s not going anywhere. The Pulse team examined locations around the country where key tech industries are booming and mapped their findings. The map shows that while Silicon Valley is the traditional home of the tech industry, there are growing tech centers around the country.

Click below to zoom.

One of the sectors spreading geographically is computing infrastructure and data services. Somerset, New Jersey, is the hub of this sector, with a significant employment increase between 2023 and 2024. Dense fiber networks and proximity to financial clients in New York City make New Jersey an ideal location for this sector. However, Ada County, Idaho, and a few counties in Maryland also support this sector.

As for custom computer programming services, the biggest hub is in Norfolk City, Virginia. There are several major software firms there, supported by the Norfolk Innovation Corridor, a “technology zone” that includes businesses, public works, hospitals, and universities. Tech startups here earn major tax incentives and other benefits. Georgia and Maine have growing centers of custom programming services too.

Software publishing is booming in the state of Texas. In Bexar, Texas, employment in this sector had doubled. San Antonio and Austin are also full of software publishing companies. Pittsburgh emerges as a hub for software publishing too, thanks to the University of Pittsburgh.

Web search portals and information services have a home in the New York City metropolitan area, particularly in Union and Essex counties. Multnomah County, Oregon, home of Portland, also has a healthy number of companies in this sector, along with many other types of creative and digital media companies.

Semiconductors are commonly manufactured in Williamson County, Texas, north of Austin. Samsung made a $17 billion investment in a semiconductor facility in Taylor, Texas, making the area a leader in the industry. NVIDIA, located in Santa Clara County, California, is another leader in this industry.

From Ohio to Maine, it’s clear that California doesn’t have the tech industry on lock. Many other cities have responded to the booming economy supported by thriving tech companies. Many cities have been totally revolutionized thanks to a major tech company opening its headquarters there. Tech businesses bring skilled workers with money to spend on many other local industries, so many communities welcome these companies with open arms.

Students and entrepreneurs can use data and maps like this to pinpoint where they may want to relocate for their job search or startup. Overall, this map offers a fascinating way to look at the state of the American tech industry by shifting our focus away from Silicon Valley and considering how tech could impact other states and cities in the future.

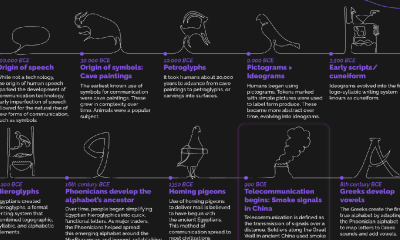

Before we used banks, barcodes, or Bitcoin, humans still developed sophisticated point-of-sale systems to exchange something of value with a stranger. We’ve reinvented solutions time and again over human history, and the team at Qualtrics created a timeline that shows us the story of this history is a lot more dramatic than your tap-to-pay transaction suggests.

Trading between humans began with the exchange of goods rather than coins or paper. Livestock, pelts, and food were the stuff of life, the most valuable items we could possess. There was no central authority to set prices and values for these things, so trades were negotiated on a case-by-case basis. The first move toward abstraction came with the exchange of goods for cowry shells and tally sticks. An interesting fact: cowry shells have been found across continents, even among civilizations that never met each other.

A major currency turning point in the ancient world was Mesopotamia’s clay tokens, used to exchange for grain and to pay off debts. Ancient Egyptians expanded on this with labor tokens that existed in a tiered system as an early form of payroll. The Code of Hammurabi, from 1750 BC, established complex rules governing credit, debt, and contracts. Economic regulation is a lot older than many people may assume.

When the Silk Road opened in 138 BC, goods, currencies, and ideas traveled thousands of miles. Muslim merchants created sakk, a document that ordered banks to pay a third party, so they didn’t have to travel with heavy coins. The sakk is the direct ancestor of a check. The Song Dynasty of China created a system of paper receipts called jiaozi, which became the world’s first paper currency.

During the Industrial Revolution, James Ritty created the mechanical cash register to help secure coins and bills from untrustworthy cashiers pocketing spare change. He called the machine, “the Incorruptible Cashier.” The Diners Club card, introduced in 1950 by American Express, became the first plastic credit card. A pack of Wrigley’s Juicy Fruit gum became the first product with a barcode scanned at the checkout in 1974.

The digital age brought about the most dramatic and rapid development. In 2009, Square turned smartphones into point-of-sale registers. This dramatically lowered barriers to entry for small businesses everywhere that could process QR codes and contactless payment methods to sell goods and services. The newest advances are in the realm of biometrics. Michigan businesses started using payments triggered by eye recognition in 2023.

From clay tokens to retinal scans, we’ve come a long way in economic innovation. These advances and technologies tell the story of humans creating solutions to the problem of developing enough trust to trade with strangers. The timeline also shows us how commerce is so tightly woven into human history and development. Some may say it’s the keystone, the foundation of human civilization. This piece is an entertaining and informative visual tale of the development of money, sales, and trade.

-

Business Visualizations2 years ago

Business Visualizations2 years agoEverything Owned by Apple

-

Business Visualizations1 year ago

Business Visualizations1 year agoAmerica’s Most Valuable Companies Ranked by Profit per Employee

-

Business Visualizations1 year ago

Business Visualizations1 year agoThe Biggest Fortune 500 Company in Every State

-

Business Visualizations11 months ago

Business Visualizations11 months agoThe Biggest Employers by Industry

-

Timelines1 year ago

Timelines1 year agoTimeline Charts the Development of Communications Technology

-

Charts2 years ago

Charts2 years agoHow Many Crayola Crayon Colors Are There? A Lot.

-

Business Visualizations6 months ago

Business Visualizations6 months agoThe Largest Companies in America That Are Still Run by the Person Who Founded Them

-

Maps2 years ago

Maps2 years agoA Map to Gold and Silver